India's First Unbiased,

Conflict-free Insurance Rating

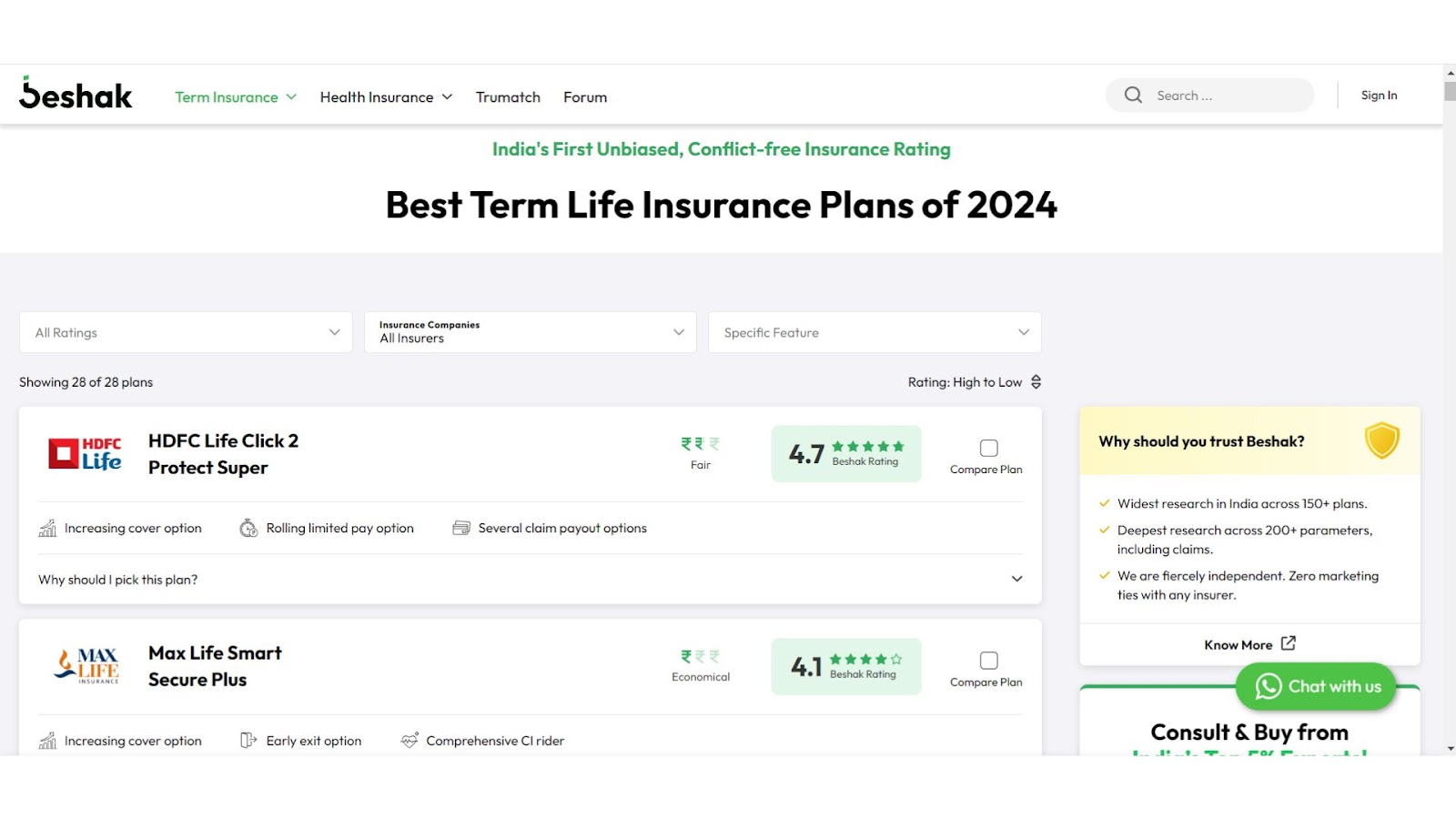

Best Term Life Insurance Plans of 2025

All Insurers

Rating: High to Low

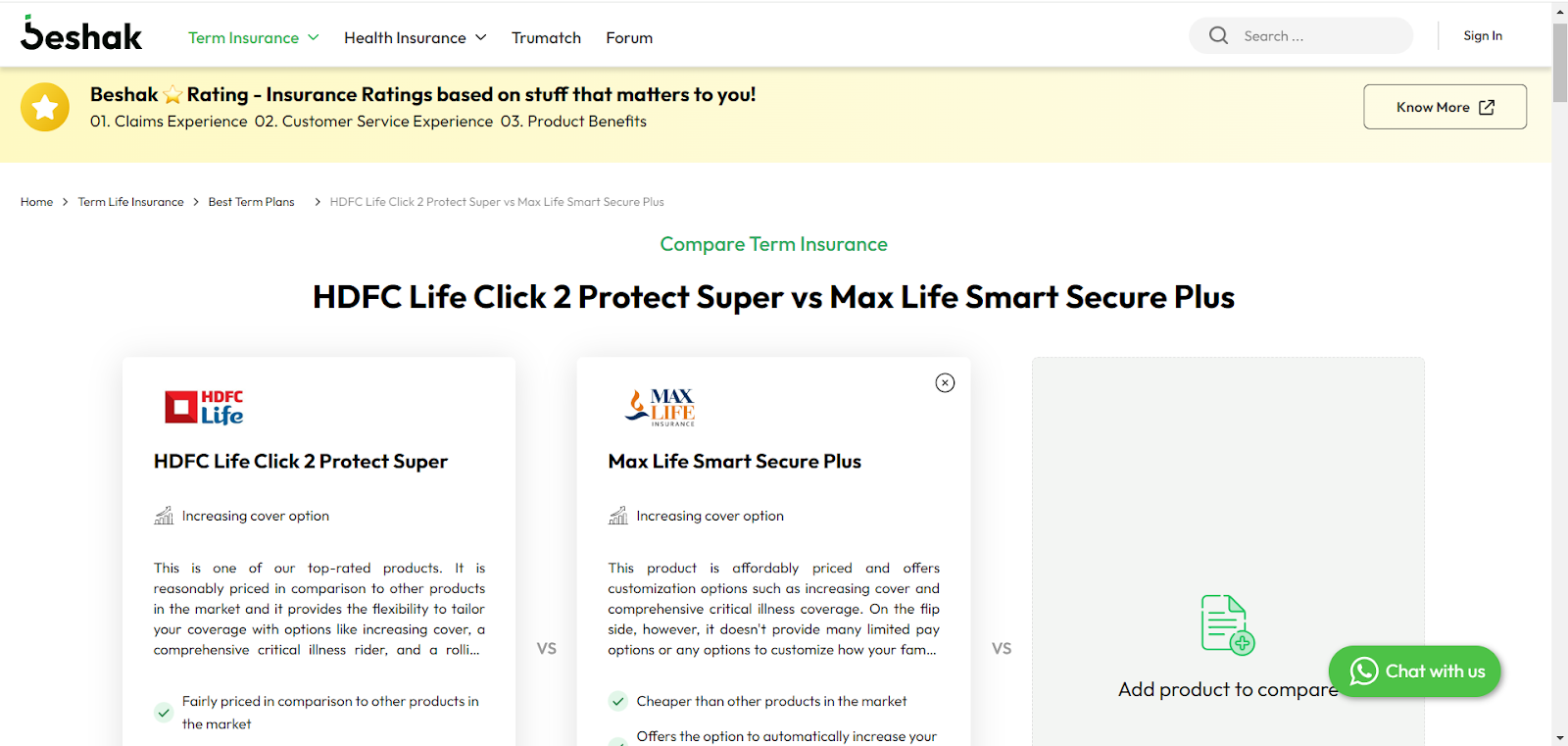

HDFC Life Click 2 Protect Super

Compare Plan

Increasing cover option

Rolling limited pay option

Several claim payout options

Canara HSBC Young Term Plan

Compare Plan

Increasing cover option

Early exit option

Several claim payout options

Axis Max Life Smart Secure Plus

Compare Plan

Increasing cover option

Early exit option

Comprehensive CI rider

Insurance isn’t one-size-fits-all. Talk to real experts before you decide.

Just comparing plan features won’t help — what works for one may not work for you. Get a free consultation with India’s top 5% insurance experts. (Not call centers. Not freshers.)

TATA AIA Sampoorna Raksha Supreme

Compare Plan

Comprehensive CI rider

Whole life cover option

Several claim payout options

Canara HSBC iSelect Smart360

Compare Plan

Increasing cover option

Early exit option

Several claim payout options

Did you know

Know the in & out of these plan.

Consult real professional experts.

Health insurance can be tricky, but you don’t have to figure it out alone. Speak with India’s

top 5% IRDAI-certified experts and choose the right plan with clarity and confidence.

Compare Plans

Add 2 more plan to compare

Term Insurance is a type of life insurance plan that pays a guaranteed sum of money to your family in case of your unfortunate death during the term of the policy. It is the easiest and most cost-efficient way to ensure that all your family’s financial needs are taken care of, in your absence. Beshak helps you find the best term insurance plan tailored to your needs and requirements!

A term insurance plan provides financial security to the family in the unfortunate demise of the policyholder. A death benefit is paid to the appointed nominee only if the death occurs during the term of the policy. If the policyholder survives the term, no maturity benefit is paid. The best term plan will safeguard your family against any kind of loans/ liabilities you’ve taken in case you pass away, and help them to maintain their standard of living by financially indemnifying them. Further, the premiums for term plans are very cheap compared to other life insurance products.

Why should you compare Term Insurance Plans?

There are no second thoughts about the fact that term insurance is one of the best insurance plans you can invest in, if you have any family member that relies on the money you make, for their expenditures.

However, term insurance plans vary from insurer to insurer and are based on several factors such as - features, benefits, premiums, customer service, claims experience, reliability, and drawbacks. Purchasing a term insurance policy that suits you and your family’s financial needs is an important decision you’ll have to make for your family’s future.

Hence, doing some research and a proper comparison is necessary to choose the right policy for you. Beshak helps you compare best term insurance plans so you can pick the plan that's suited to your unique needs!

Compare Term Insurance Plans 2025 From Beshak

Choosing the best term insurance plan can make you feel like you're at a crossroads and don't know which way to go. We provide the ideal remedy in this situation. Our term plan comparison page is here to help you make an informed decision. You can find the top term insurance options for 2024 that are customised to meet your specific needs by following a few easy steps.

Here's how to use Beshak to achieve it quickly -

👉Step 1: Access Beshak

Go to beshak.org to access Beshak's main website first. You will find the option "Term Insurance" in the upper left corner of the webpage.

👉Step 2: Begin Your Comparison

Under the drop-down list after clicking “Term Insurance”, choose the option "Compare Term Insurance."

👉Step 2: Select And Compare Plans

Choose two or three plans to compare side by side. You can click on ‘Compare Now’ and then evaluate the features, pros and cons of each option, or simply refer to Beshak’s expert ratings for guidance.

👉Step 3: View The Comparison Table

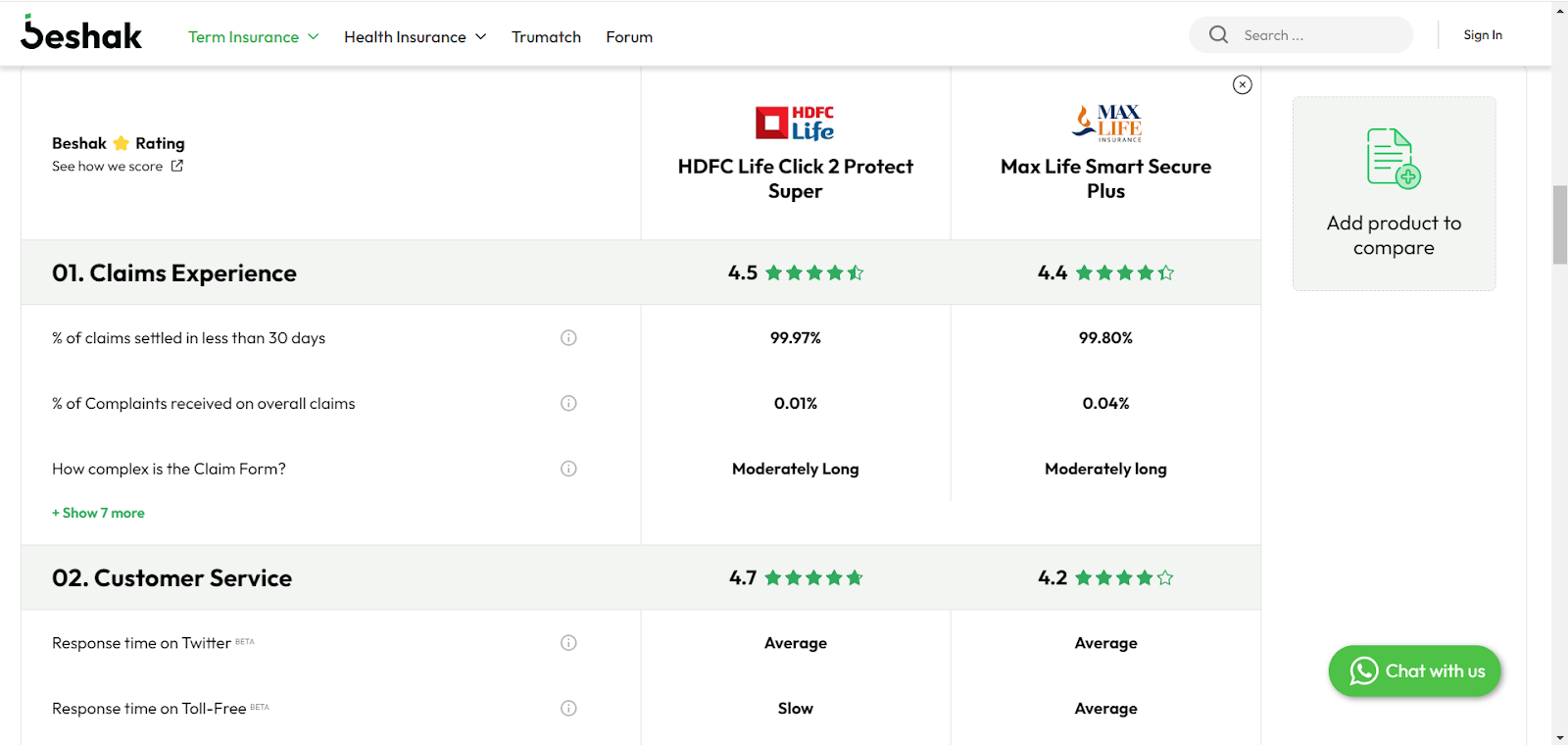

Let’s say we compare the HDFC Life Click 2 Protect Super plan and the Max Life Smart Secure Plus plan. Following your selections, a comparison table will show up. The table highlights the key differences between the plans, focusing on factors like cost-effectiveness, market reputation, product details, and additional coverage enhancement options.

You can easily compare term plans using Beshak ⭐️ Rating, which takes into account key factors like claim experience, customer service, and product benefits. Each of these important metrics is explained in detail below, helping you make an informed choice.

👉Step 4: Evaluate The Customer Service & Claims Experience

Next, you’ll want to assess the claims experience by reviewing several key criteria, including:

- Home pickup service for claim documents

- Online claim tracking system

- Availability of a personal relationship manager for claims

- Separate forms for claims over three years

- The Solvency ratio of the insurer

- Percentage of claims settled within 30 days

- Percentage of customer complaints related to overall claims

- Complexity of the claim form

- Claim settlement ratio (the number of claims settled)

- A dedicated toll-free service for claim-related queries

- Response time on toll-free and Twitter

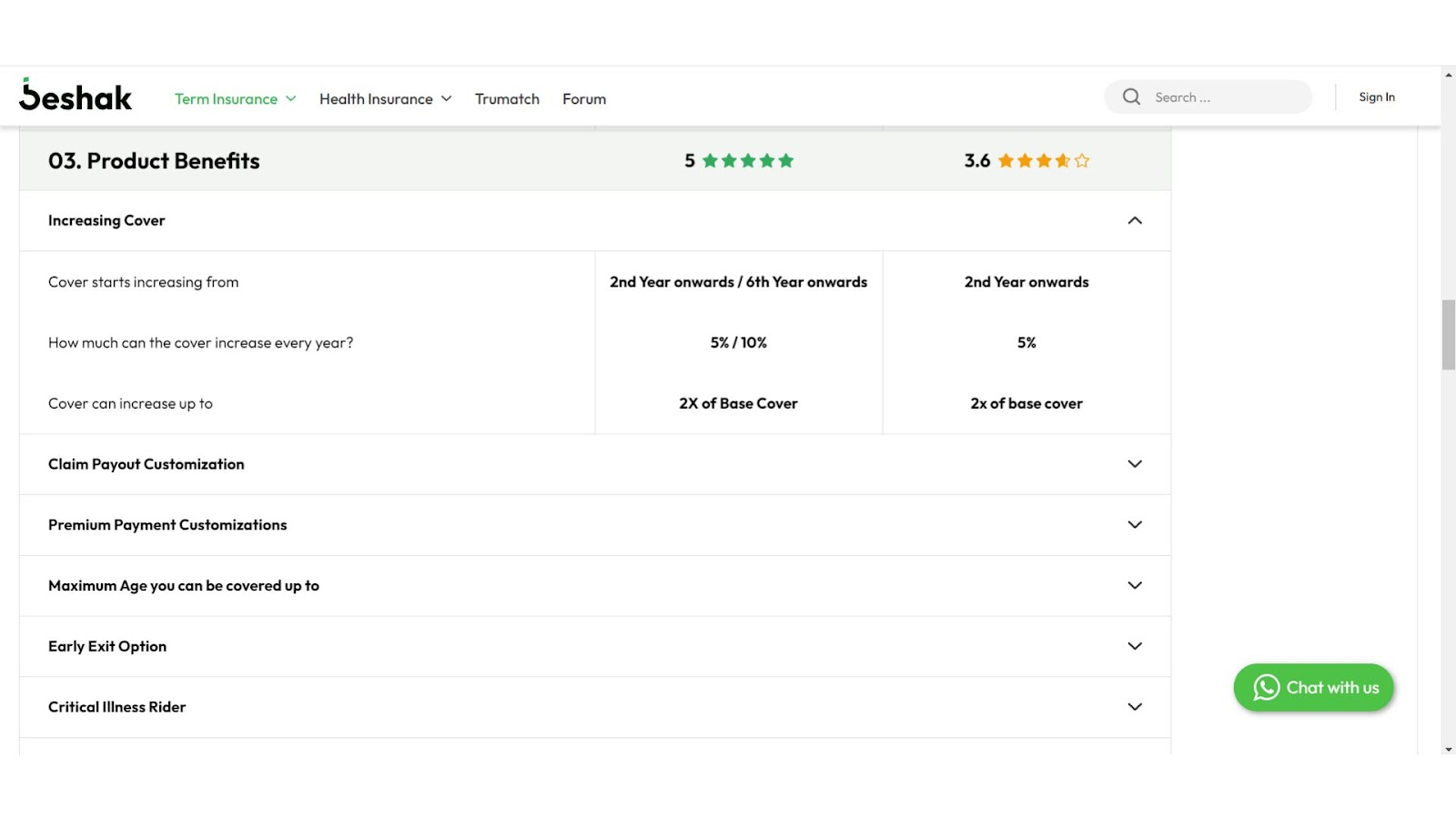

👉Step 5: Consider Product Benefits

While making the call, consider factors such as customer service, rider choices (Critical Illness, Waiver of Premium, Accidental Death Benefit), limited pay options, early exit opportunities, and product benefits (such as increasing cover or customising claim payouts).

Beshak's distinctive advantage is that it provides you with more options to consider by suggesting different term insurance options available in the market.

👉Step 6: Review The Final Analysis

Beshak offers a comprehensive analysis that covers the claims track record, customer service experience, and product benefits once you've compared the plans.

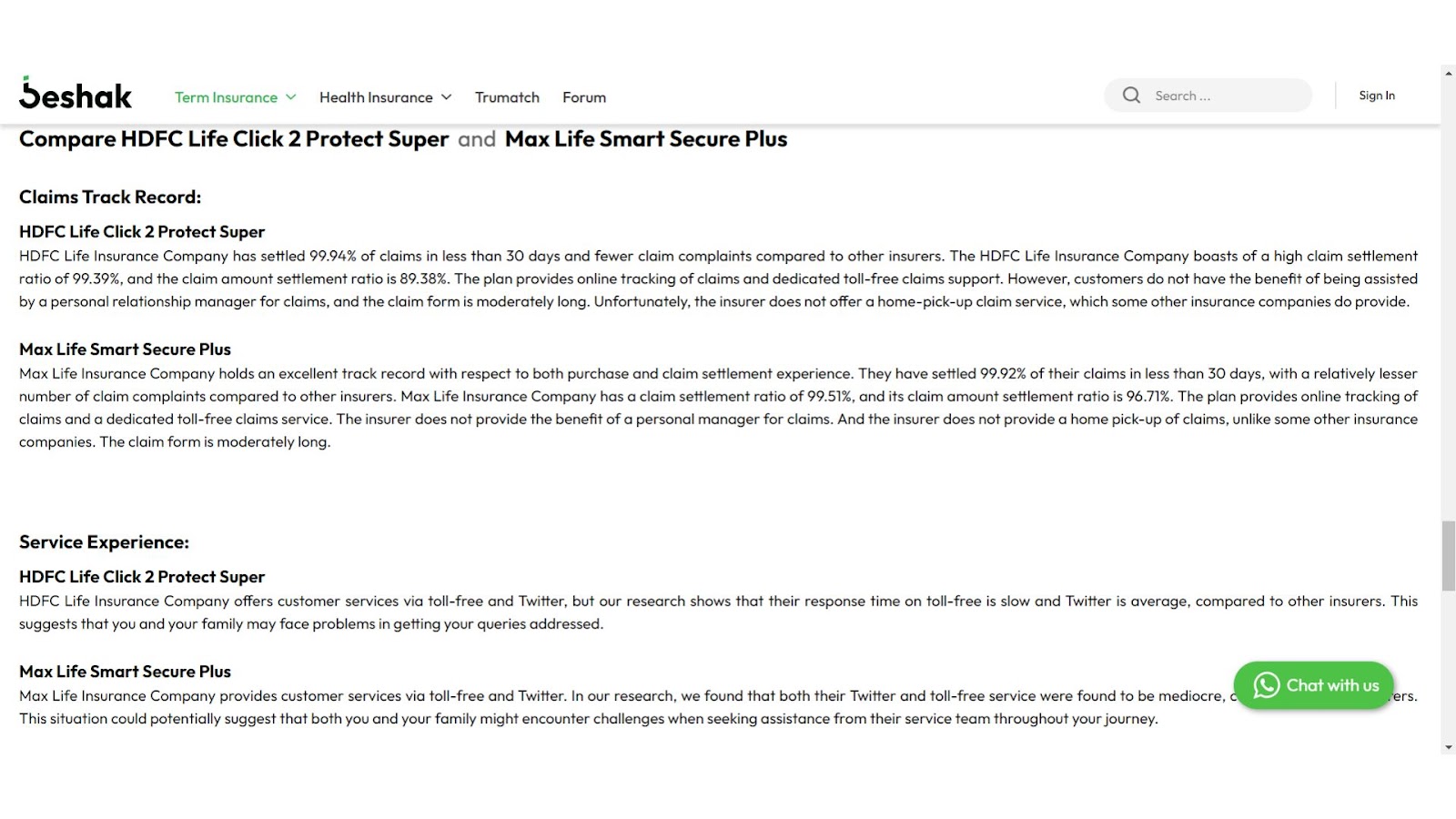

For a complete analysis of the HDFC Life Click 2 Protect Super plan and Max Life Smart Secure Plus Plan, click the link here.

The information provided is all reliable and updated as on June 2024. It has been gathered from public disclosures found on the websites of insurers and the IRDAI.

Why Should You Compare Term Insurance Plans Before Buying?

Selecting a term insurance policy is among the most crucial financial decisions you will ever make. Ultimately, term insurance acts as a layer of protection, guaranteeing your family's financial security in case of your untimely passing. It's important to compare term insurance choices because there are a lot of insurers offering various plans. Here are a few reasons this step is crucial -

☑️Examine And Comprehend Your Options For Coverage

Although safeguarding your family's finances is the main objective of all term insurance policies, there can be major differences among them. Plans differ in terms of cover amount, policy benefits, and additional features. Some plans may also offer extra toppings such as critical illness cover, accidental death benefits, or waiver of premiums rider. Thus, by comparing different plans, you can quickly find out which policy offers the perfect balance of benefits tailored to your specific needs.

☑️Picking The Most Affordable Premiums

The premiums often becomes one of the most prominent factors when choosing a term insurance plan. For the same cover amount, different insurers may offer various kinds of premium prices. By comparing these prices, you can locate a plan that fits your requirements on a budget without compromising the coverage your family requires.

☑️Examining Personalised And Flexible Payment Methods

Term insurance policies vary not just in terms of rates but also in terms of flexibility and customisation in premium payments. You can choose regular or limited payment terms with certain plans, while others provide the option of single-premium payment. Many insurers even allow you to decide how often you want to pay - whether monthly, quarterly, or annually. By comparing options, you can find a plan with payment terms that best suit your financial preferences and lifestyle.

☑️Ensuring An Adequate Sum Assured

The amount your beneficiaries would get in the awful scenario of you passing away, also known as sum assured, is one of the most important components while making the choice.

The number varies based on your lifestyle, any existing commitments, and your long-term financial objectives.

Certain insurance policies guarantee larger amounts at competitive rates, while others might not meet the required amounts. By using Beshak Comparison tools, you can obtain the right amount of coverage that fits your family's needs without going over budget by comparing several plans.

☑️Unlocking Additional Benefits And Riders

Adding riders like accidental death cover, disability benefits, critical illness, etc cover can significantly raise the value of your term insurance policy. Nevertheless, it's crucial to remember that not all plans include the same riders, and the price of these add-ons might vary greatly between providers. Through a comparative analysis of different term insurance policies, you can be certain that the riders and extra benefits offered meet your unique requirements and that you won't overpay for aspects that are important to you.

Beshak Comparisons- Your Path To Peace

In the ultimate sense, getting term insurance is all about giving you and your dear ones peace of mind. You can minimise future worries and disappointments by taking the time to compare term insurance policies. This will help you feel a little more confident in your choice. You must carefully consider your alternatives in order to select the finest plan for your particular scenario since your family's financial security is too essential to leave to chance. By using this deliberate approach, you can ensure that your loved ones are receiving the security they need.

Options to customise Term Insurance Plans

📌 Limited Pay Option

- If you want to finish paying off all your premiums in shorter and faster installments before the maturity of your policy, you can select the limited pay option while purchasing your policy. Limited pay will help you to get the payment liability off your chest quickly.

📌 Purchase Riders

- As you get close to finishing your term insurance customizations, you’ll often hear about riders. Riders are add-ons that you can buy for a very low price along with your term insurance plan and get additional benefits under specific conditions. Though purchasing riders that are sold with term plans might seem attractive, it would be more beneficial if you take a comprehensive cover for most riders.

📌 Flexible Payment Options

- Term insurance allows you to choose from multiple premium payment options. You can choose from among the following options - limited pay, single pay, or regular pay. If you choose limited or regular pay, you can pay the premiums either monthly, quarterly, half-yearly, or annually according to your convenience.

📌 Multiple Payout Options

- Term insurance plans offer multiple payout options for claim settlement and allow you to configure how your family will receive the claim amount - as a one-time payout or as monthly income installments. Depending on your purpose for purchasing the term insurance policy and your nominee's financial knowledge, you can decide the best term insurance plan that will be beneficial for your family and you can also decide how they receive the money.

📌 Tax Benefits

- Term insurance plans offer tax benefits too. The premiums paid for term insurance plans are eligible for tax deductions under Section 80C of the Income Tax Act. Tax benefits can also be availed on the amount received by the nominee under Section 10(10D) of the Income Tax Act.

Key Features of a Term Insurance Plan

Term insurance is one of the best insurance policies available in the market today. Here are some key features of a term insurance plan:

👉 Easy to Buy

- Buying a term plan is comparatively easier than buying other types of insurance products. The framework is simple: you just need to calculate the appropriate cover amount as per your family’s financial objectives, the standard of living, and any loans/ liabilities. You need not be bothered about what returns will you get, where the company will invest your money, etc.

👉 Affordable Plan

- Affordability is one of the most remarkable features of a term insurance plan. Compared to other life insurance products, the premiums of term plans are very low and hence, do not create a hole in our pockets.

👉 The Convenience of Paying Premiums

- Most term insurance plans offer flexibility to pay premiums annually, half-yearly, quarterly, or monthly. They also offer single pay or limited pay premium payment. As per your budget and your convenience, you can choose the payment option that is the most appropriate for you.

👉 Flexible Payout Options

- Term insurance offers multiple payout options - lump-sum, lump-sum + monthly income, only income. Based on your purpose of purchasing the term plan, your loans/liabilities, and your nominees’ financial aptitude, you can choose the most suitable payout option.

How to choose the Best Term for your Term Plan?

The right duration for a term insurance plan may vary for every individual depending upon their financial situation. Here are some factors that you should consider while buying a term plan:

- Loans/ Liabilities

- You should consider the loans/ liabilities which your family will have to repay in the case of your untimely demise and the time it would take for those loans/ liabilities to be settled while deciding the term of a term insurance plan. For instance, if you’ve taken a home loan that has to be settled in 15 years, your policy term should not be less than 15 years or else your family wouldn’t have an adequate cover amount to settle all the loan you've taken.

- Financial Dependents

- If your financial dependents are young, the term of your plan must ideally be the duration till they become financially capable to support themselves. You must also take into account other major events like paying for your child’s higher education, wedding, etc while deciding the terms of your policy. Even if you are not around during these times, you can ensure that your term policy can financially provide for your family and their needs are still taken care of

- Affordability

- The premiums for term insurance can vary widely based on the insurance company you choose. Further, policies with a longer duration could be more expensive than short-term insurance plans. Hence, while deciding the term for your term plan, you must first consider whether you can afford to pay the premiums over a longer period or not.

Best Term Insurance Plans in India - FAQs

☝️ What is the minimum income to buy Term Insurance?

- If you want to invest in a regular term insurance plan, at present you should have an annual income of at least Rs. 2 lakhs, however, these rules keep changing from time to time.

☝️ Can I get myself insured under the Term policy if I have diabetes?

- Insurers look at each proposal on a case-to-case basis. You should be upfront about your health condition and provide all available documents, records required - ensuring transparency before you buy the policy.

☝️ Do I need to declare myself as a tobacco user if I smoke occasionally?

- Even if you smoke occasionally, you should declare yourself as a tobacco user because if you try to withhold information and the insurer finds out about it later, he may charge an extra premium. The insurer might even cancel your policy and deny the policy benefits.

☝️ Why are premium rates higher for smokers than non-smokers?

- Compared to non-smokers, smokers have higher chances of getting cancer and other smoking-related ailments which increases the risk of early death. Since the possibility of a claim is higher in such cases, premium rates to are higher for smokers than non-smokers.

☝️ What would happen if I start smoking or consuming alcohol after the policy issuance?

- Your base policy cover will not get affected if you start smoking or consuming alcohol after the policy is issued. As per the terms & conditions of the policy, there is no requirement to inform the insurer about it.

☝️ If a person dies outside India, will the nominee still receive the death benefit?

- If the policyholder dies during the policy term, the nominee is entitled to receive the death benefit compensation, irrespective of the place of death of the policyholder.

☝️ Can I change the duration of life cover after the policy is issued?

- No, you cannot change the duration of life cover after the policy is issued. Purchasing a fresh policy with a longer duration is the only option if you want to increase the policy duration.

☝️ Can I increase my Sum Assured after the policy is issued, during the policy tenure?

- If you buy your policy with the life stage benefit or the increasing cover feature, you can increase your sum assured during the policy tenure, after the issuance of the policy. Otherwise, a manual upgrade will involve buying an additional, separate term insurance plan.

☝️ Is it possible to add a rider to my existing term policy?

- While some insurers allow riders to be added only at the time of buying the policy, some insurers allow you to add a rider to your existing policy after charging a nominal cost.

☝️ How much time does it take to settle any claim?

- The procedure of claim settlement varies from insurer to insurer. As per IRDA guidelines, the insurer must settle the claim within 30 days after all the necessary documents are submitted.

☝️ Can we claim Term Insurance from two companies?

- If you have disclosed complete details of your first policy to the insurance company from whom you have purchased the second policy, you can claim term insurance from two companies.

☝️ What is underwriting?

- Underwriting is the process by which institutions or individuals take up financial risk in exchange for some price. It involves evaluating the proposal, assessing the risks, establishing proper premiums, and taking responsibility for a policy by agreeing to pay in case of any damage or loss.

☝️ Can I change my nominee after the issuance of the policy?

- Yes, you can change your nominee after your term insurance policy has been issued. You can contact your insurer and ask him about the process to do so. Mostly, all you need to do is fill out the nomination form and submit it to your insurer.

☝️ What is Section 45 of the Insurance Act?

- Section 45 of the Insurance Act safeguards the interests of the policyholders. It states that a life insurance company cannot reject or deny any claim, for any reason after 3 years of issuing the policy.

☝️ Do life insurance companies check my medical history? What medical conditions will affect my term insurance premiums?

- Yes, insurance companies check your medical history when you apply for the policy. Your premium rates might be affected if you or your family have a medical history of life-threatening or chronic diseases, or if your present medical condition indicates a future health issue.

Term Products Comparison