India's First Unbiased,

Conflict-free Insurance Rating

Best Health Insurance Plans of 2025

All Insurers

Rating: High to Low

HDFC Ergo Optima Secure

Compare Plan

No room rent limit

All day care procedures

2X cover from Day 1

Tata AIG MediCare Premier

Compare Plan

No room rent limit

All day care procedures

Consumables coverage

ICICI Lombard Elevate

Compare Plan

No room rent limit

All day care procedures

Reduced PED waiting period

What is Beshak

Rating?

Rating?

Reliance General Health Gain (Power)

Compare Plan

No room rent limit

All day care procedures

Reduced PED waiting period

Reliance General Health Infinity

Compare Plan

No room rent limit

All day care procedures

Consumables coverage

HDFC Ergo Optima Restore

Compare Plan

No room rent limit

All day care procedures

Consumables coverage

Bajaj Allianz My Health Care

Compare Plan

Single Private AC Room

399 day care procedures

Consumables coverage

Tata AIG MediCare

Compare Plan

No room rent limit

541 day care procedures

Consumables coverage

ICICI Lombard Health AdvantEdge

Compare Plan

Single Private Room

All day care procedures

Consumables coverage

Aditya Birla Activ One (MAX)

Compare Plan

No room rent limit

All day care procedures

Consumables coverage

Aditya Birla Activ Assure Diamond

Compare Plan

No room rent limit

586 day care procedures

Consumables coverage

Royal Sundaram Lifeline (Supreme)

Compare Plan

No room rent limit

All day care procedures

Organ donor expenses cover

Aditya Birla Activ Fit (Preferred)

Compare Plan

No room rent limit

All day care procedures

Consumables coverage

Royal Sundaram Multiplier

Compare Plan

No room rent limit

All day care procedures

Organ donor expenses cover

Star Health Super Star

Compare Plan

No room rent limit

Fixed premium till you claim

Consumables coverage

AB Activ Health Platinum (Premier)

Compare Plan

No room rent limit

586 day care treatments covered

Day 1 coverage for few PEDs' management costs

Niva Bupa Aspire (Titanium+)

Compare Plan

No room rent limit

All day care procedures

Fixed premium till you claim

Bajaj Allianz Health Guard (Platinum)

Compare Plan

No room rent limit

399 day care procedures

Organ donor expenses cover

Niva Bupa ReAssure 2.0 (Titanium+)

Compare Plan

No room rent limit

All day care procedures

Fixed premium till you claim

Niva Bupa Health Companion

Compare Plan

No room rent limit

All day care procedures

Health check-up from day 1

Care Insurance Care Supreme

Compare Plan

No room rent limit

All day care procedures

NCB up to 600%

Star Health Assure

Compare Plan

Any room except Suite

All day care procedures

Consumables coverage

Star Health Comprehensive

Compare Plan

Any room except Suite

All day care procedures

Consumables coverage

Care Insurance Ultimate Care

Compare Plan

No room rent limit

All day care procedures

Reduced PED waiting period

Star Health Family Health Optima

Compare Plan

Any room except Suite

All day care procedures

Consumables coverage

Women Care

Compare Plan

Any room except Suite or above

All day care procedures

Spouse's mid-term inclusion

Manipal Cigna PH Prime (Advantage)

Compare Plan

No room rent limit

All day care procedures

Consumables coverage

Manipal Cigna ProHealth (Plus)

Compare Plan

Any room except Suite

546 day care procedures

NCB up to 200%

Care Insurance Care

Compare Plan

Single private AC room

541 day care procedures

Consumables coverage

New India Floater Mediclaim

Compare Plan

Up to 1% of SI per day

139 day care procedures

Spouse's mid-term inclusion

Why should you trust Beshak?

Widest research in India across 150+ plans. Deepest research across 200+ parameters, including claims. We are fiercely independent. Zero marketing ties with any insurer.

Widest research in India across 150+ plans. Deepest research across 200+ parameters, including claims. We are fiercely independent. Zero marketing ties with any insurer. Know More ![]()

Compare Plans

Add 2 more plan to compare

Why Should You Buy The Best Health Insurance Policy In India?

Getting your hands on the top-notch health insurance policy in India is a must for a bunch of reasons. Let’s discuss all about it below -

👉Rising Medical Expenditures

Healthcare expenditures are on the rise. A decent health insurance policy helps cover these fees, ensuring you obtain the necessary treatment without financial burden.

👉Extensive And Broad Coverage

The best policies come packed with comprehensive coverage, spanning hospitalisation, pre- and post-hospitalisation care, daycare procedures, and sometimes, even outpatient treatments.

👉Cashless Services

Many of the top-rated health insurance plans have tied up with a large number of hospitals so that you can get cashless treatment wherever you go.

👉Tax Benefits

Good news: According to section 80D of the Income Tax Act, health insurance premium payments can help reduce your taxable income. This is like getting a tax break while ensuring good health!

👉Better Access To High-Quality Healthcare

You don't have to worry about paying for high-quality medical care at reputable facilities when you have a solid health insurance policy.

👉Financial Security

When unexpected medical bills hit you out of nowhere, health insurance steps in like a real lifesaver for your wallet. In any health crisis, it keeps your hard-earned savings from vanishing into thin air.

👉Additional Advantages

The best health insurance plans come with other benefits, including free annual medical check-ups, coverage for complementary medicine, maternity care, etc.

👉Coverage For Lifestyle Conditions

As lifestyle-related diseases like diabetes and hypertension become more prevalent, having health insurance becomes increasingly crucial. This suggests that you can deal with such circumstances without being hindered by money problems.

Feeling a bit lost on where to dive into the health insurance maze? No worries, we've got your back. Let's take a journey together to uncover the secrets of finding that ideal health insurance plan just for you.

When Should You Buy Health Insurance?

Well, you should get health insurance before you get into an accident or contract a serious health condition that necessitates a major hospitalization. Insurance companies find it risky to cover someone who has a lifestyle disease since this will lead to more hospitalizations, and hence, more claims. They may either charge an extra premium or levy some additional conditions. In a nutshell, you should be covered by health insurance as soon as you are born till you die - either through your parent's policy, employer's policy, spouse's policy, or your own policy.

How To Select The Best Health Insurance Policy?

Here’s a simple guide for you to choose the best policy for you-

✅Look At Your Specific Needs

You have to decide the type of health insurance you need based on some factors i.e. age, the size of your family, medical history and current health problems.

✅Compare Different Plans Online

Assess several health insurance policies by using online comparison tools. Compare the premiums, coverage benefits, exclusions, and claim settlement ratios.

✅Coverage

Look for a health insurance plan that covers more than just hospital stays. Think broadly: pre- and post-hospitalization, daycare procedures, ambulance costs, and the entire shebang should be covered.

✅Network Hospitals

Make sure to review the insurer's network of hospitals offering cashless treatment. A broad network means you'll have a wider range of top-notch healthcare facilities to choose from when you need them.

✅Sum Insured

Make sure there is enough sum insured to cover any future medical costs. When determining the quantity of coverage, ensure that inflation and growing healthcare expenditures are taken into account.

✅Waiting Period

Examine the waiting periods for those special treatments and pre-existing conditions. Shorter periods are crucial; you wouldn't want to be stuck waiting when you urgently need care.

✅No Claim Bonus

Seek for plans that offer a no claim bonus, which gradually adds more coverage by raising your sum insured each year you go claim-free.

✅Look Into The Exclusions

Take some time to understand the policies' exclusions. Make sure the policy does not exclude any necessary treatments or ailments for which you may require additional coverage.

✅Premiums

Affordability matters, but cutting corners on coverage to save money isn't the way to go. It's quite essential to strike a balance between the benefits offered and the premium cost.

✅Riders And Add-Ons

To boost your coverage, you can think about including add-ons or riders like maternity coverage, critical sickness coverage, or personal accident coverage. Extra protection at just a small cost! How cool is that?

✅Customer Support

Examine the customer service offered by the insurer. During emergencies, having prompt and effective customer service can make a world of difference.

✅Policy Terms

To comprehend the coverage, exclusions, and claim procedure, thoroughly read the terms and conditions of the policy document.

Ready to dive into finding the perfect health insurance plan that's got your health and wallet covered? Stick around to uncover all the awesome perks waiting for you!

Compare Health Insurance Plans 2025 From Beshak

Are you ready to explore your options for health insurance? You can visit Beshak.org to access the official Beshak website.

Step 1 - Head To Beshak Website

- Open your browser and visit Beshak.org.

- Once there, click on the "Health Insurance" option at the top of the website.

Step 2 - Select “Compare Health Insurance”

- In the Health Insurance menu, select "Compare Health Insurance" to access a variety of available plans.

- Here, you’ll find some of the newest and best plans from reputable insurers.

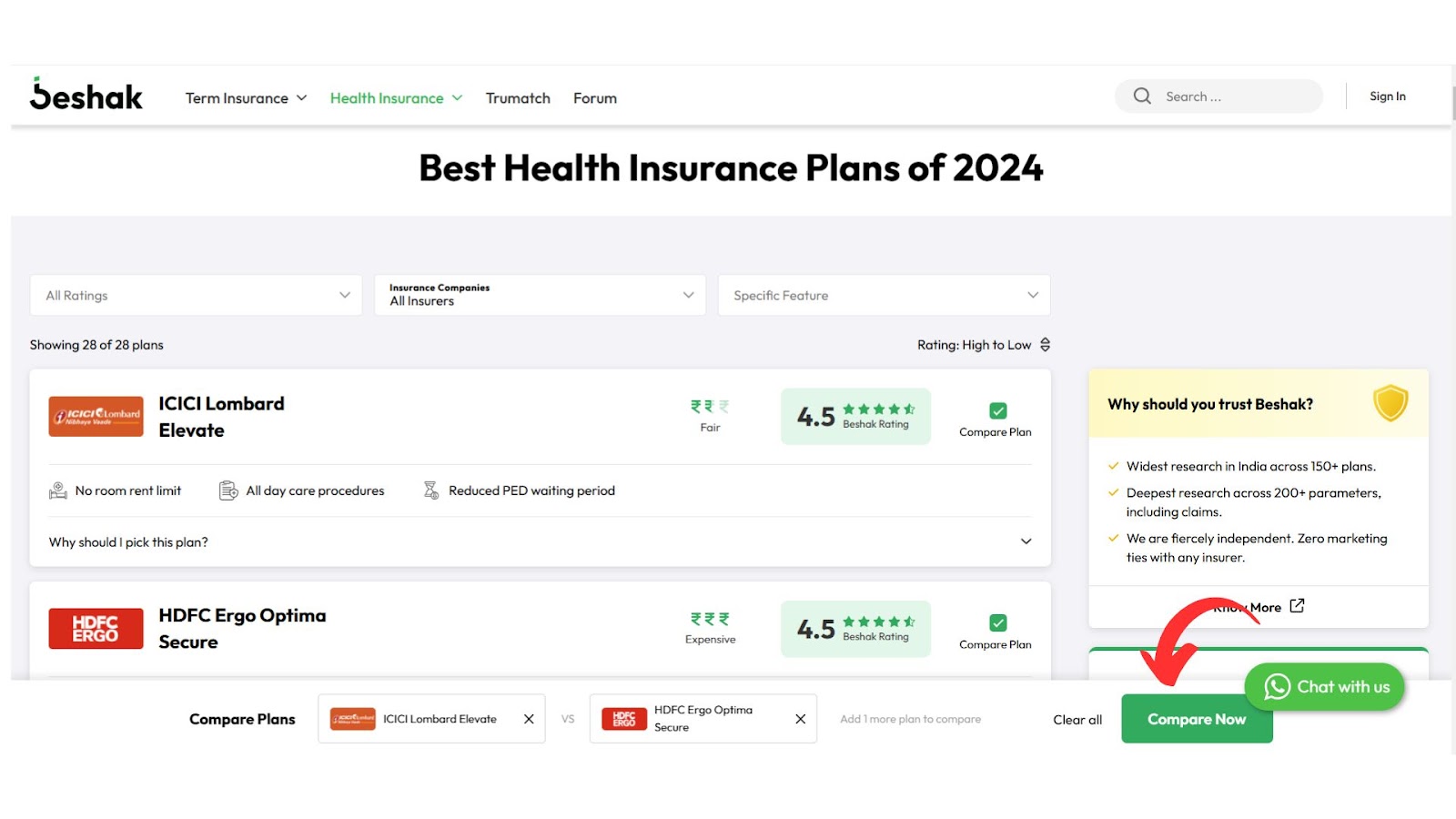

Step 3 - Pick Your Plans For Comparison

You can choose to compare plans from 2 to 3 insurance providers.

Options to filter plans include -

- Beshak Ratings: Based on Beshak’s expert ratings.

- Your Preferred Providers: Go with the insurers you’re interested in.

- Key Features: A dedicated update is on the way to filter plans prioritising specific benefits or limits.

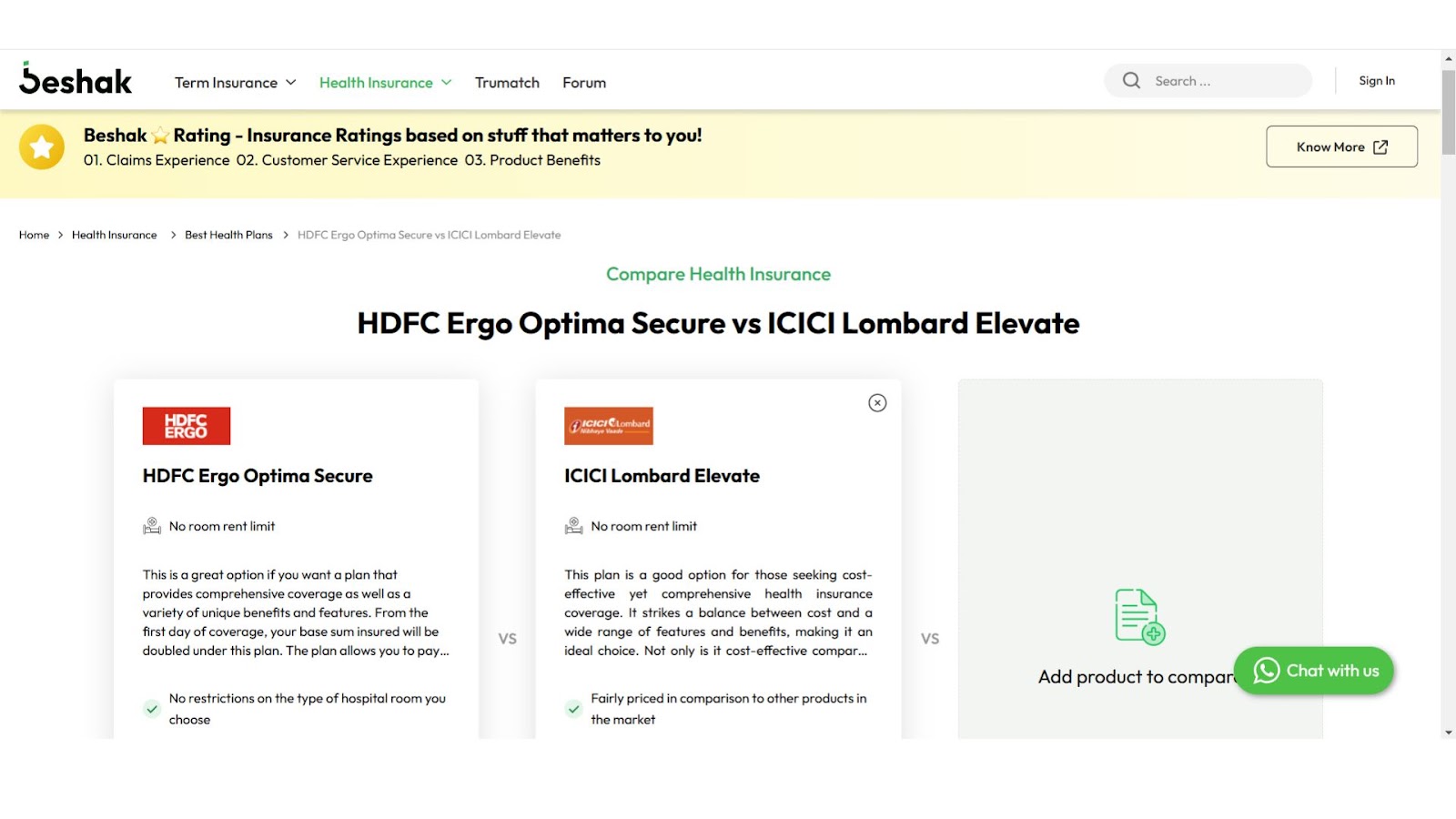

Step 4 - View A Detailed Comparison Table

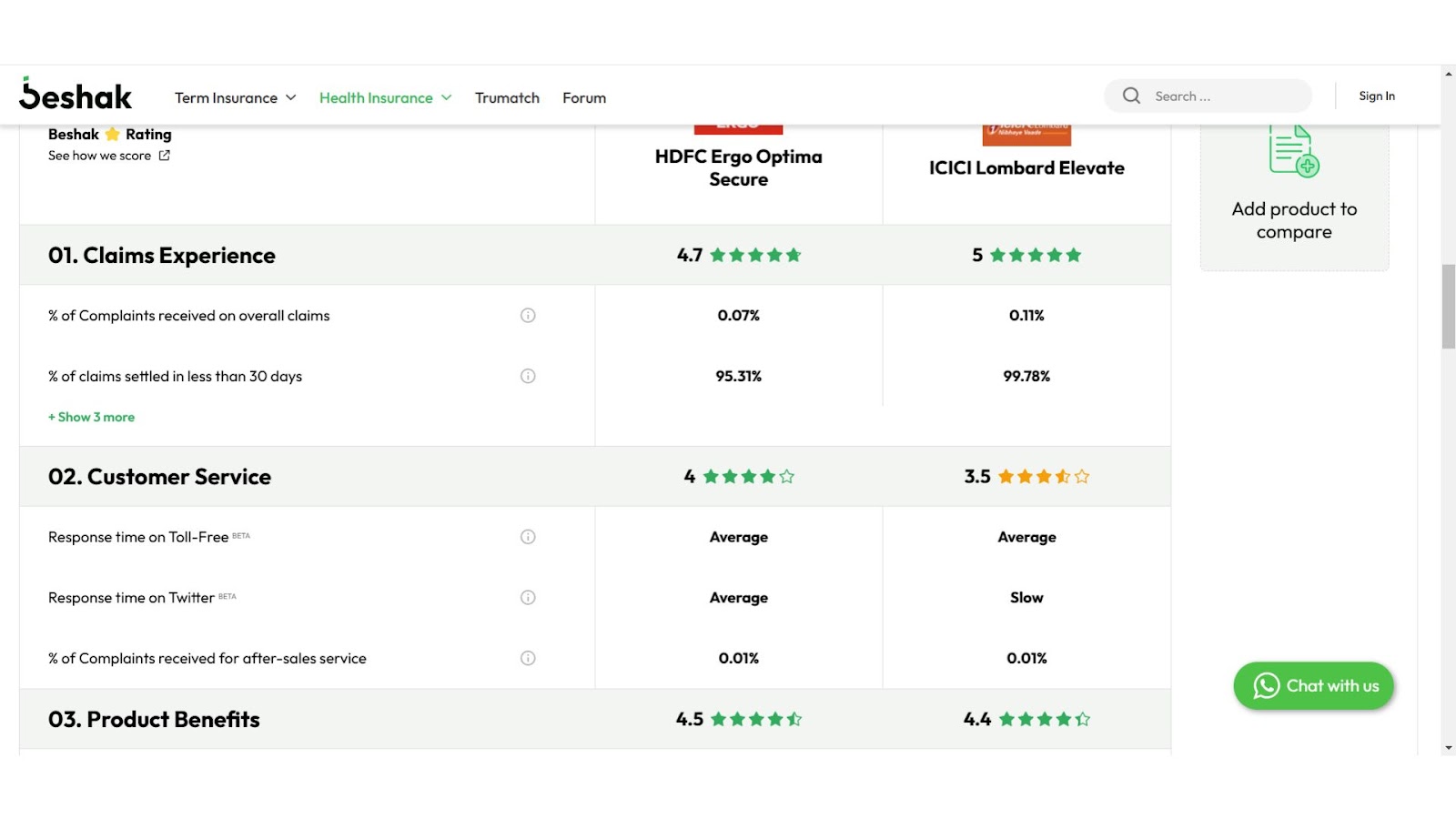

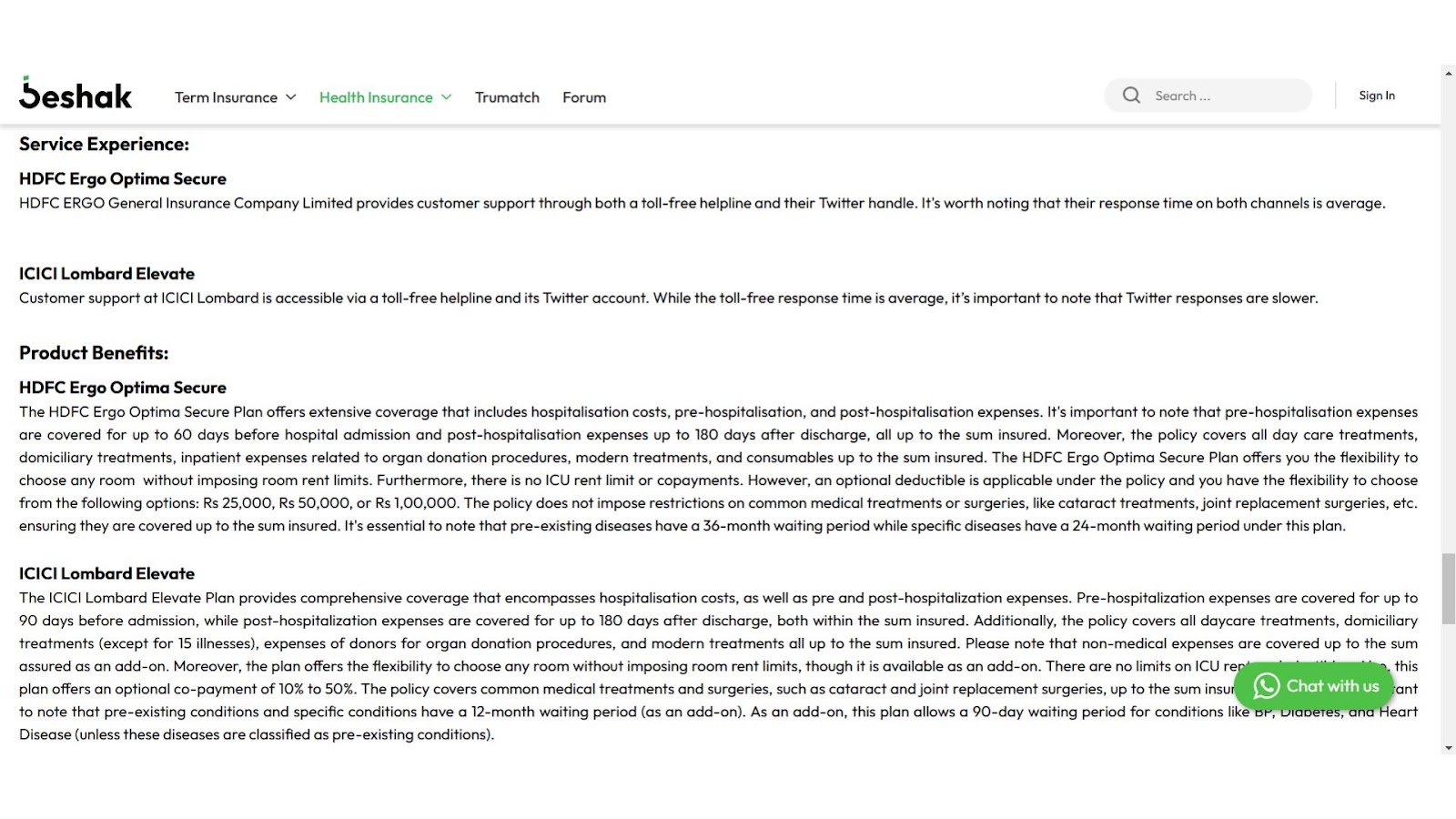

Let’s, for example, compare ICICI Lombard Elevate and HDFC Ergo Optima Secure plans. Once you’ve selected the plans, Beshak generates a comparison table that highlights the main differences.

Step 5 - Learn More About Claims & Service Experience

Scroll down for a detailed analysis of each plan. Here, you’ll find data on certain metrics such as -

- Claims Experience

- Product Benefits

- Limits and exclusions

- Customer Service

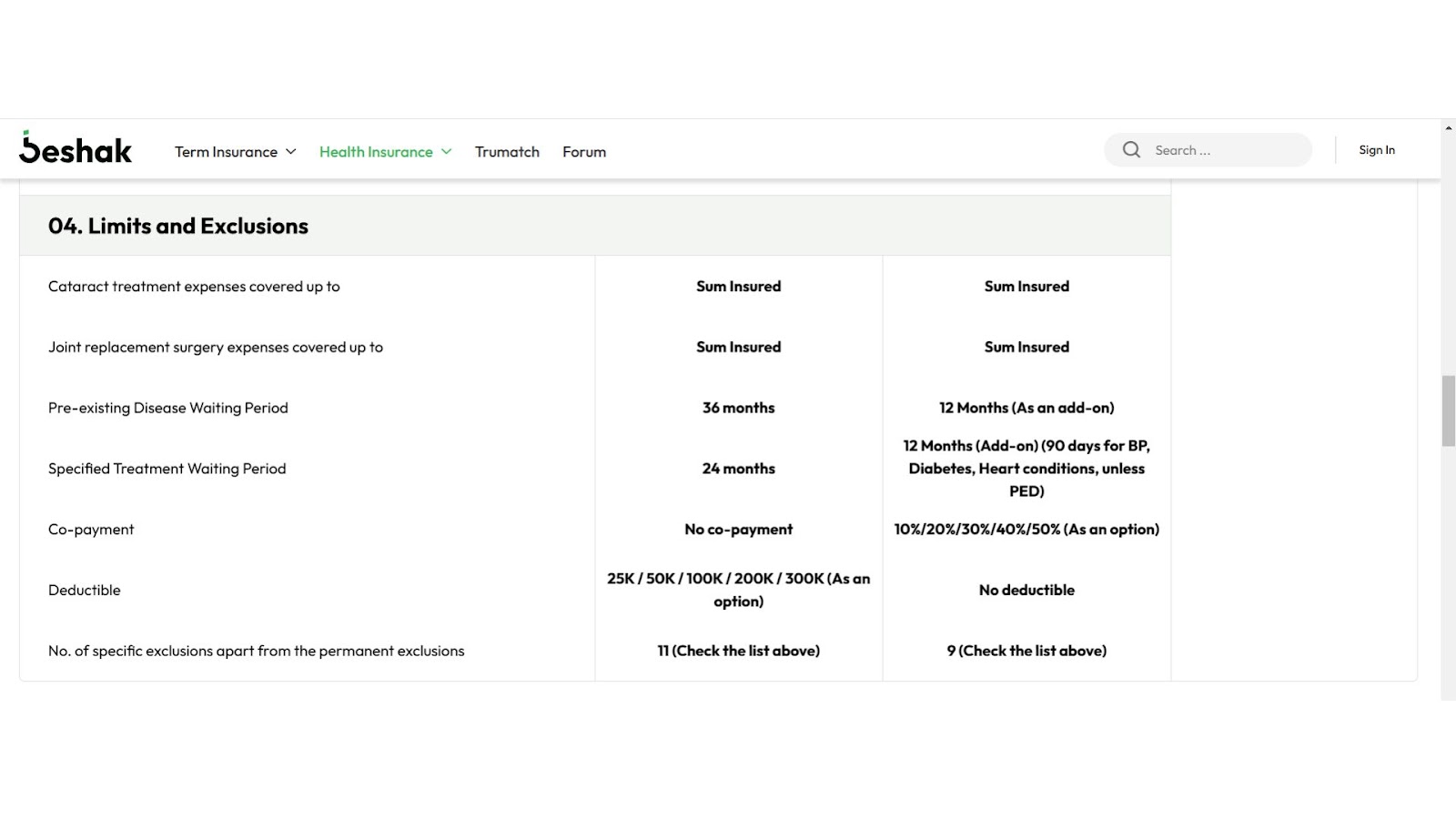

Step 6 - Explore Key Benefits And Coverage Options

Each plan's detailed comparison includes a breakdown of benefits -

- ICU and Room Rent Limits for hospitalisation.

- Pre- and Post-Hospitalization Coverage for tests, follow-ups, etc.

- Daycare and Domiciliary Care for treatments that can be done within 24 hours or at-home treatments.

- Organ Donor Benefits for transplants.

- Modern Treatment Coverage for advanced procedures.

- No Claim Bonus that rewards healthy periods without claims

- Refill Benefit for restoring sum insured after it has been exhausted due to claims.

- Non-Medical Expense Coverage for items like syringes, gloves, etc.

Step 7 - Understand Waiting Periods, Co-Payments, And Exclusions

It is also equally important to familiarise yourself with limitations -

- The different types of Waiting Periods.

- Co-payment requirements.

- Permanent and Temporary Exclusions.

Final Tip: Take Your Time To Compare

Beshak's tools are designed for thorough decision-making, so explore each feature and data point to ensure you’re making an informed choice.

For more information on the comparison between ICICI Lombard Elevate and HDFC Ergo Optima Secure plans, check the link here. You can dive even deeper into plan details and find answers to any health insurance questions you have at Beshak.org.

It's crucial to remember that Beshak advises against centering your choice exclusively on the claim settlement ratio.

The chance to compare the plans you've chosen with similar deals from different insurance companies is just another amazing feature of Beshak.

In this manner, the choices you make will come out more comprehensively to you. Last but not least, Beshak offers thorough details on the plans you've chosen, including past claims history, client experiences, and product benefits.

Please Note: All data and information provided are up-to-date and sourced directly from insurance company websites, including public disclosures, policy documents, brochures, and the IRDAI website.

Why Should You Compare Health Insurance Plans Before Buying?

A critical step that should never be skipped in the process of finding the best health insurance is comparing policies.

You can make sure that the plan you choose precisely suits your needs by taking the time to carefully consider and evaluate all of your options. This methodical approach offers you peace of mind and financial security in addition to assisting you in striking the ideal balance between cost, coverage, and flexibility.

Remember that the choices you make now can have a long-term effect on your well-being later. Let's explore the main reasons why comparison is so important.

▶️Find Coverage That Meets Your Specific Needs

Since every person has distinct health needs, it's critical to evaluate plans that are customised for your specific situation. As you explore your options, look for policies that cover -

- Pre-Existing Conditions: Many plans include specific T&Cs regarding pre-existing conditions. To ensure that you are protected when you need it most, it is imperative that you find one that takes account of your medical history.

- Specialised Treatments: Verify that the plan covers all vital procedures, chronic illness management, maternity care, or other treatments specific to your circumstances. Make sure to study these services because standard policies may not always cover them!

▶️Keep An Eye On The Cost-Effectiveness

Let's face it- finding an affordable option is very important because health insurance may be a substantial expense. Take into account the following elements while comparing plans -

- Premiums: Take into account the amount you must shell out each month or each year for your coverage. This will help you gauge how it fits into your budget.

- Deductibles: This is the amount you must pay by yourself before your insurance coverage kicks in. Knowing this can help you avoid future unanticipated expenses.

- Out-Of-Pocket Expenses: Examine copayment rates for out-of-pocket expenses. Your overall healthcare costs might be substantially lower if you are aware of the cost of using healthcare services.

Finding options that balance price and critical coverage is crucial when looking for health insurance policies. Seniors, in particular, need to know this because they often need healthcare.

▶️Understanding The Significance Of Policy Sub-Limits

It's important to know that many health insurance policies have sub-limits before delving in. Let's take a closer look at these limits, as they have the potential to greatly affect your entire coverage -

- Be Mindful Of Room Rent Limits: Room rent limits are a key consideration to be mindful of. Some plans may restrict the amount you can claim for room rentals during hospitalisation. This may result in more upfront expenses if you require a more expensive room or a longer stay.

- Check The Ambulance Service And ICU Caps: Keep in mind the limitations of ICU and ambulance service. It's vital to confirm that your policy provides sufficient emergency coverage because the costs in these circumstances can mount up rapidly if they are not covered.

▶️Assessing Add-On Benefits

Add-on benefits for health insurance can be quite important for improving your coverage and giving you peace of mind. Let's look at a few of the most popular add-ons that you might want to take note of -

- Consider Critical Illness Insurance: When certain serious illnesses are diagnosed, this benefit pays out in full, providing financial support when you need it most. It serves as a safety net that helps lessen stress in trying circumstances.

- Don’t Overlook Maternity Benefits: Prenatal and postnatal care are included in this coverage, which can be very expensive for many families. Having this add-on will guarantee that you receive the assistance you require during your pregnancy.

- Outpatient Treatment: Certain insurance policies also provide coverage for outpatient care. This can be crucial for treating persistent medical conditions since it enables you to get the care you need without having to pay for expensive hospital visits.

▶️Learn from Customer Reviews

Spend some time reading consumer reviews as you consider the benefits of a plan . Studying other policyholders' experiences with their claims procedures can provide you with important information about the dependability and quality of customer care provided by the insurer.

▶️Claims Assistance: Help When You Need It

Lastly, check if the insurer offers dedicated assistance with claims. When it comes time to file a claim, having committed support can help you feel more secure by streamlining the claims process.

▶️The Importance Of Flexibility And Renewability

Flexibility is crucial when selecting a health insurance plan, particularly when your medical demands change over time. Let's look at some crucial factors to think about in the field -

- Understanding Your Renewability Options: You must make sure to look at renewability options. Selecting a plan that can be renewed indefinitely without requiring major modifications to the terms or coverage is essential. This guarantees that as you get older, you can continue to be protected without facing any unforeseen restrictions.

- The Need for Adjustable Terms: Following that, think about the policy's adjustable terms. Search for policies that let you adjust the coverage to suit your evolving medical requirements. This is especially crucial for senior citizens, who might need more assistance and care as they grow older.

- Assessing The Network Of Hospitals And Providers: When choosing a health insurance plan, accessibility to a wide network of hospitals and healthcare providers is just as important as flexibility. Here are a few crucial things to remember -

- Evaluating In-Network Facilities: Check the in-network facilities listed in the plan first. Verify if a wide variety of hospitals and clinics are covered by the insurance policy, specifically those that you have a preference for or are conveniently located close to. This can help you avoid wasting time and stress when seeking care.

- Cashless Treatment Options: A major financial relief during emergencies is provided by the cashless hospitalisation that many plans provide at network hospitals. This advantage lets you concentrate on your recuperation rather than worrying about up-front payments.

Ensuring Access to Specialists: Lastly, confirm that visits to specialists are covered by the plan and that their services are included in the network. Receiving comprehensive care that is suited to your needs is made easier when specialists are accessible to you at no extra cost.

Benefits Of Purchasing The Best Health Insurance Plan In India

Apart from offering access to high-quality treatment and financial protection, purchasing the best health insurance plan in India has several other advantages, which include -

👉Comprehensive Coverage

The best health insurance policies cover a wide range of expenses related to hospital stays, pre- and post-hospitalisation, daycare treatments and even outpatient care. This guarantees that you will be financially protected against a variety of medical expenditures.

👉Cashless Treatment

The top health insurance plans have tie-ups with many hospitals, so they can offer you cashless services. This means the insurance company will take care of the bills directly with the hospital, so you can focus on getting back on your feet!

👉Tax Benefits

Did you know paying premiums for health insurance can actually lower your taxable income? Thanks to Section 80D of the Income Tax Act. It's a great way to save money while protecting your health!

👉Financial Protection

Health insurance shields your finances from being depleted by expensive medical bills. It pays for costs associated with procedures, therapies, prescription drugs, etc., ensuring you don’t experience financial strain during medical emergencies.

👉Protection For Critical Illnesses

Severe conditions, including kidney failure, cancer, heart disease, etc. are usually covered by the top plans. You can address significant health disorders with the financial support you need, thanks to this specific coverage.

👉Coverage For Maternity And Newborns

Maternity costs and neonatal care are covered by certain health insurance plans. This might be especially helpful for young families who intend to start a family.

👉Preventive Healthcare

Preventive health check-ups, immunisations, and wellness initiatives are often covered by top insurance plans. Regular check-ups help catch health issues early and improve overall health management.

👉Alternative Medical Therapies

Alternative treatments like Ayurveda, Homoeopathy, and other traditional treatments are covered by certain plans, offering a comprehensive approach to healthcare. So, you get the best of both worlds!

👉Ambulance Charges

Picture a scenario where you're dealing with a medical emergency and the added strain of arranging an ambulance. Luckily, numerous health insurance plans include coverage for emergency ambulance charges, alleviating the financial burden during times when urgent medical help is needed.

👉Hospital Cash Allowance Per Day

A daily monetary allowance is provided by certain policies for each day a patient is hospitalised. This helps themhandle expenses over and above hospital charges like meals and family members’ transport expenses.

👉Global Coverage

Certain premium health insurance plans provide global coverage, guaranteeing protection wherever your travels may lead.

👉Obtaining High-Quality Healthcare

A solid health insurance plan opens doors to top-tier healthcare services at prestigious hospitals, guaranteeing you receive the best care possible whenever you need it.

Selecting the right insurer is as vital as choosing the perfect plan. It forms the backbone of your healthcare security, ensuring you're covered when it matters most. Dive into our detailed guide below to make the best choice!

How To Choose The Best Health Insurance Company?

When selecting the finest health insurance supplier in India, many factors must be taken into consideration with caution. Below is a simple guide to help you with making a knowledgeable decision -

✅Reliability And Reputation

Check out how the insurance company rolls in the industry. Find those big players with a solid rep and a history of coming through for folks like you. Dive into reviews and ratings from current policyholders to feel know how satisfied they are.

✅Network Hospitals

Check the network hospitals on the insurer's list. A robust network ensures you can get cashless treatment at renowned hospitals nationwide. Be sure to check if there are hospitals near your home for added convenience.

✅Range Of Plans

Choose a provider that offers various health insurance options crafted for unique needs, including maternity plans, critical illness plans, senior citizen plans, individual plans, and family floater plans. Having a myriad range of options allows you to choose a plan that fits your needs perfectly.

✅Benefits And Coverage

Check what the insurance provider offers in terms of benefits and coverage. A comprehensive policy should address hospitalisation, pre- & post-hospitalisation, daycare procedures, and ambulance costs, among other things. And don’t forget to explore other benefits, such as wellness programs, preventive health checkups and no-claim bonuses.

✅Affordability And Premiums

Compare the costs of similar coverage offered by various insurers side by side. Make sure the premiums are within your budget without sacrificing essential benefits. For long-term coverage, look for discounts and flexible payment choices.

✅Customer Service

Customer service plays an important role, particularly during times of medical contingencies. Look for an insurance company that is known for its ability to offer timely and efficient customer service. Verify if it offers round-the-clock helpline as well as claim status tracking, online chat support , among others..

✅Claim Process

Make sure the insurer makes claiming straightforward and transparent. Look for a quick settlement process with minimal paperwork—check for important features like cashless claims enabling direct settlement with hospitals in their network.

✅Waiting Periods And Exclusions

Get a grip on what's not covered and how long you'll wait for certain things. Pick a provider with fewer exclusions and shorter waiting period coverage for pre-existing diseases and specialised treatments.

✅Renewability

Make sure the insurer allows for lifetime renewals. This is especially crucial since as people age, their medical needs also increase.

✅Add-Ons And Riders

Look into whether the insurer provides extra riders and add-ons such as critical illness covers, personal accident protection, maternity benefits, and more. These can bolster your basic policy and offer additional security.

Health Products Comparison